Inside the Moscow Real Estate Surge as Prices Drop to 303,000 Rubles per Square Meter

Moscow Real Estate Sees Surge in Market Activity as Prices Drop to 303,000 Rubles Per Square Meter

A Notable Shift in the Capital’s Residential Landscape

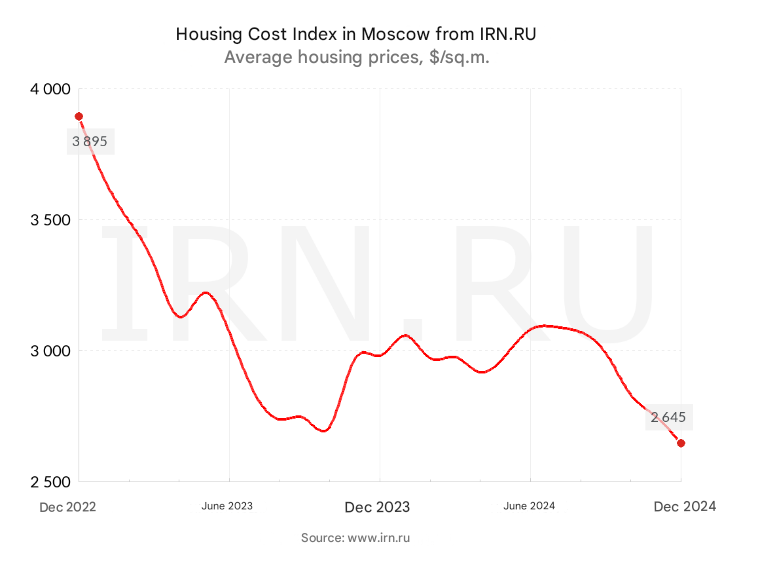

The latest figures reveal a striking adjustment in the Moscow property market as the average price for residential space has tumbled to 303,000 rubles per square meter within just a week. This development marks a departure from recent trends where values remained steady or edged upward, raising fresh questions about the trajectory of the metropolitan housing sector. The new pricing data underscores the evolving dynamics in one of Russia’s most closely watched property environments, with potential implications for both buyers and sellers operating in the heart of the nation’s capital.

Understanding the significance of this price dip requires familiarity with the structure of the urban residential market. Moscow’s real estate has historically been seen as a haven of both stability and robust growth, driven by strong demand, continual urban migration, and concerted development efforts. The “price per square meter” metric acts as the industry’s pulse, enabling swift comparisons across property types and locations. For years, adjustments at this scale have signaled deeper transformations, whether tied to seasonal shifts, lending environment changes, or broader economic influences.

Key Market Influences Behind Recent Price Fluctuations

Several interconnected factors are contributing to the notable reduction in listed values. One pivotal aspect relates to the volume of available offerings and the pattern of new projects entering the market. Recent quarters have seen developers in Moscow’s core hesitate to launch fresh projects, a trend attributed to both the expense and accessibility of financing. As fewer new properties become available, shifts in supply exert pressure on overall price dynamics, causing movement in the average square meter cost.

Simultaneously, there has been a recognizable ebb in demand for mass-market properties, particularly in entry-level and economy-class segments. Market observers have reported declines in both the number of residential lots available and the total transactional volume within this segment. With fewer buyers entering the arena and more owners considering liquidation, established price points are naturally under revision to stimulate activity and maintain liquidity. Meanwhile, secondary factors such as long-term mortgage rates and the general cost of borrowing continue to shape affordability thresholds and the willingness of prospective homeowners to enter the market.

Milestones and Core Terminology Shaping the Market

To contextualize the fresh price benchmark, it is essential to grasp core concepts that professionals use in the Moscow real estate sphere. The “primary market” describes sales direct from developers, while the “secondary market” covers previously owned properties changing hands. The “economy,” “comfort,” and “premium” classifications set expectations for finishings and location, guiding both buyers and analysts as they interpret pricing shifts and sales data.

Recent years have seen pronounced fluctuations in these categories. At the upper end, luxury properties have attracted resilient demand, even as the broader market softens. Conversely, limitations in the economy and comfort segments have driven both inventory reductions and price recalibrations. Tangible milestones include phases where growth in per-unit sales volumes spiked in particular classes or when available choices plummeted due to development slowdowns.

Implications for Urban Residents, Investors, and Developers

The movement to 303,000 rubles per square meter sets a new reference point that all market participants must now adjust to. For current residents considering a change in living arrangements, the development may open new possibilities to “trade up” or secure more space at a previously unreachable price. Those contemplating a purchase in Russia’s capital now face a nuanced environment where timing and due diligence are more crucial than ever due to volatility in mortgage availability and project listings.

For developers, the drop heralds a period of necessary adaptation. Some may delay new launches, seeking to gauge buyer sentiment as the situation develops further. Investors, for their part, are likely to conduct a more granular analysis of individual neighborhoods, as the new price basis may reveal localized opportunities in areas with strong infrastructure or proximity to transportation hubs.

The Road Ahead for Moscow’s Residential Sector

With these price adjustments, the market is entering a phase marked by recalibration and renewed attention from both analysts and end-users. Whether this episode signals a longer-term movement or a transitory response to recent shifts in lending rates and project pipeline awaits further confirmation. Nevertheless, the 303,000 ruble average now stands as the headline indicator for a critical turning point in the city’s contemporary real estate landscape.

Market watchers and stakeholders will closely monitor new developments to determine whether this pricing marks the beginning of a broader cycle or a short-lived correction. The interplay of policy decisions, buyer preferences, and financial conditions will ultimately determine where the city’s property values settle as the year progresses.